DSCR + ADU = AWESOME

The Secret Weapon for Real Estate Investors: DSCR Loans + ADUs

If you’re looking to scale your real estate portfolio without the headache of showing your tax returns or personal pay stubs, you need to talk about DSCR loans. Throw an ADU (Accessory Dwelling Unit) into the mix, and you’ve got a recipe for a high-yield "house hacking" strategy—even if you don't live there.

What is a DSCR Loan?

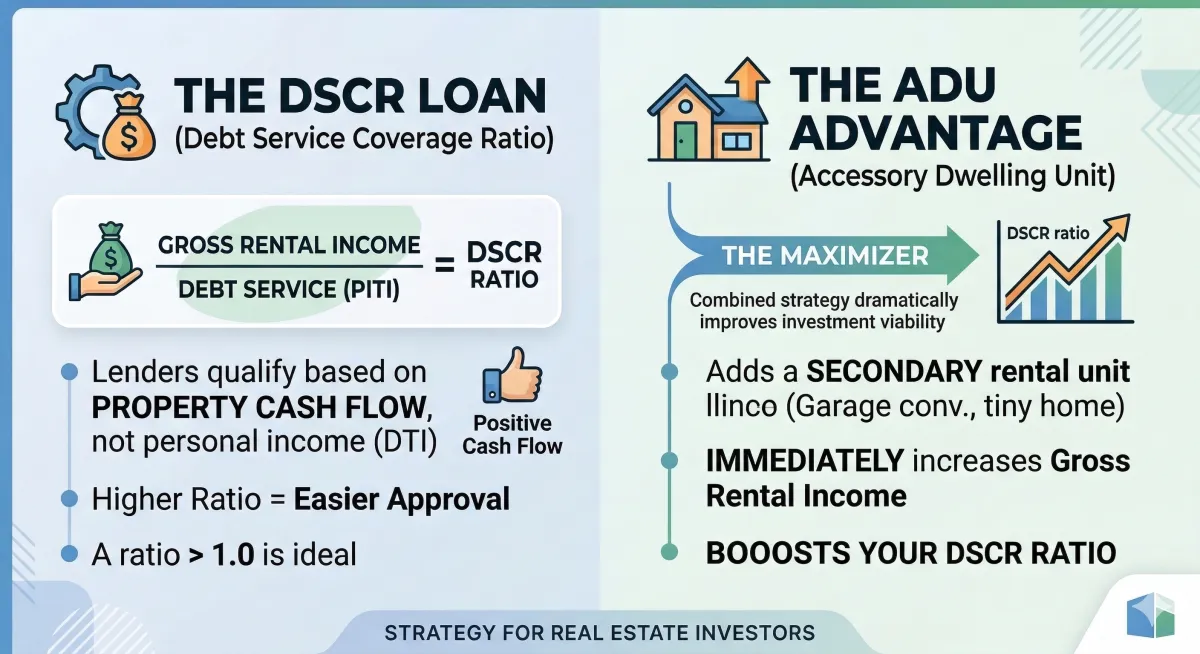

Unlike a traditional mortgage that looks at your income, a Debt Service Coverage Ratio (DSCR) loan looks at the property’s income.

Lenders use a simple formula to see if the rent covers the mortgage:

DSCR > 1.0: The property generates more income than its expenses (Positive Cash Flow).

DSCR < 1.0: The property is "underwater" on a monthly basis (Negative Cash Flow).

Most lenders look for a ratio of 1.2 or higher to account for vacancies and repairs.

The ADU Advantage: Boosting Your Ratio

An ADU—whether it's a converted garage, a basement suite, or a tiny home in the backyard—is a massive "cheat code" for DSCR qualification.

Increased Gross Income: By adding a second unit, you’re effectively doubling (or significantly increasing) your rental income without doubling your mortgage payment.

Higher DSCR Score: Since the "Debt Service" (the loan) stays relatively stable while the "Gross Rental Income" jumps up, your ratio improves. This can help you secure better interest rates or higher leverage.

Risk Mitigation: If one unit sits vacant for a month, the income from the other unit keeps your DSCR healthy and your mortgage paid.

Why Investors Love This Duo

No DTI Stress: Your personal debt-to-income ratio doesn't matter. You can have 10 other properties; as long as this one cashes out, you're good.

Speed: DSCR loans typically close faster than conventional loans because there's less "red tape" regarding your personal finances.

Density Strategy: In many states (like California), new laws make it easier than ever to add ADUs. You can turn a single-family home into a multi-unit cash cow using a single DSCR loan.

The Bottom Line

If you're eyeing a property that doesn't quite "math out" on its own, check if the lot allows for an ADU. That extra unit might be the key to hitting the DSCR numbers you need to get the deal funded.

Pro Tip: Not all DSCR lenders treat "projected" ADU rent the same way. Some want the unit to be finished, while others will consider "As-Completed" appraisals.